Introduction: When a Good Stock Suddenly Falls

Imagine Ramesh, a young working professional in Hyderabad. After months of reading about the stock market, he finally opens a demat account and buys his first shares of a well-known IT company at ₹200 per share. He feels proud. He checks the price every morning with his tea.

Three weeks later, global markets fall. IT stocks correct sharply. His stock is now at ₹160, down 20%. His ₹20,000 investment is showing a loss of ₹4,000. Nothing has changed in the company. The business is the same. The clients are the same. Only the price on the screen has changed, and so has Ramesh's peace of mind.

Now three voices start fighting inside his head. One says, "Sell now before it falls more." Another says, "Just wait, it will come back." A third whispers, "The stock is cheaper now, maybe buy more?"

This exact confusion is faced by lakhs of Indian retail investors every time the market corrects. This article answers that confusion in plain language. We will understand what a DIP in the share market really is, how buying the dip works, how averaging reduces your purchase price, and, most importantly, when this popular strategy is smart and when it is dangerous.

What is DIP in the Share Market?

In the share market, a DIP simply means a fall in the price of a stock (or the overall market) from its recent level. It is not a technical company term or a scheme. It is everyday market language for a price decline or a share market correction.

For example, if a stock was trading at ₹200 and it falls to ₹180 or ₹160, people say the stock has "dipped". If the Nifty 50 or Sensex falls a few percent over some days or weeks, people say the market is "in a dip" or "in a correction".

"Buying the dip" is a strategy built on top of this idea. It means buying or accumulating shares of a company after its price has fallen from a previous level, with the expectation that the price will recover over the long term. Instead of panicking during a fall, a dip buyer treats the lower price as a possible discount, but only when the underlying business is still healthy.

Dips happen all the time on the NSE and BSE. They can be small (2–5%), medium (10–15%), or deep (20% or more). They can happen to a single stock, a sector like banking or IT, or the entire market. Sometimes the reason is temporary fear. Sometimes the reason is a real problem inside the company. Telling the difference between these two is the entire skill of buying on dips.

Quick clarity

DIP here is not an abbreviation of any official scheme. Do not confuse it with SIP (Systematic Investment Plan), which is a regular fixed-interval investment method, usually in mutual funds. A dip is a price event; buying the dip is a response to that event.

How Buying the Dip Works

The logic of buying on dips rests on one simple mathematical idea: when you buy more shares at a lower price, your average purchase price comes down. A lower average price means the stock does not need to climb back to its old high for you to break even or make a profit.

Here is the practical shape of the strategy:

You never invest all your money at once. You keep your capital divided into parts, for example three or four portions.

You make a small first purchase in a company you have researched and believe in for the long term.

If the price falls meaningfully (say 15–20%) and the fall is due to market-wide fear rather than damage to the business, you add another small portion.

If it falls further and fundamentals are still intact, you may add carefully again, still keeping some money in reserve.

Then you wait patiently. The goal is long-term recovery, not a quick bounce.

Notice the words that keep repeating: small, carefully, researched, long term. Buying the dip is not about bravery. It is about buying quality businesses at temporarily reduced prices while strictly controlling how much money you risk at each step. This is why the strategy suits long term investing in India far better than short-term trading.

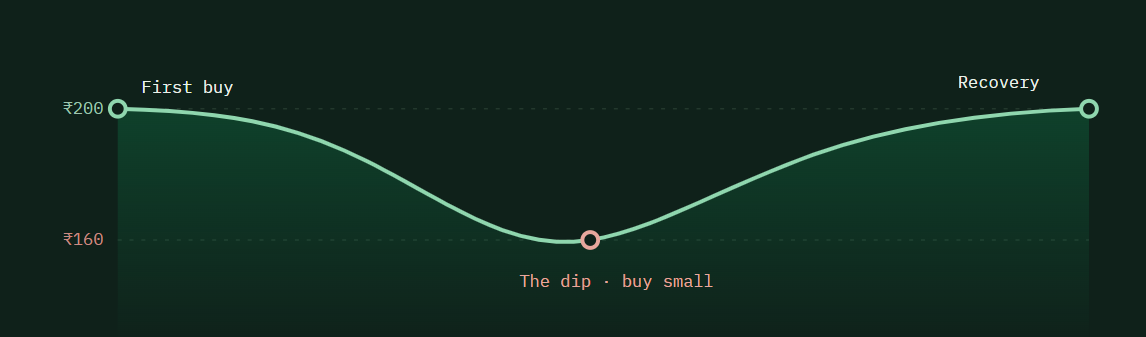

Simple Example: Wipro Share at ₹200 Falling by 20%

Let us make this concrete with a simple, educational example using round numbers. Suppose an investor buys shares of Wipro at ₹200 per share. She invests a small amount, say ₹10,000, and gets 50 shares.

A few months later, due to a broad market correction and weakness in IT stocks globally, the price falls 20% to ₹160. Her investment now shows a loss on paper. A panicking investor might sell at ₹160 and lock in a ₹2,000 loss. But suppose she has studied the company. Revenue is stable, debt is low, the business model is intact, and the fall looks market-driven, not company-driven. Instead of selling, she buys a small additional quantity, say another ₹8,000 worth (50 shares at ₹160).

Now look at her position. She owns 100 shares for a total of ₹18,000. Her average price in the stock is ₹18,000 ÷ 100 = ₹180, which is below her first buying price of ₹200.

If the price falls again, she does not rush. She re-checks the business. If fundamentals are still strong, she may accumulate carefully with one more small amount, keeping the rest of her capital safe. If something has genuinely broken in the company, she stops adding, no matter how "cheap" it looks.

Later, if the stock recovers to ₹200, she is not just back at break-even like a person who bought everything at ₹200. She is in profit, because her average price is ₹180. At ₹200, her 100 shares are worth ₹20,000 against a cost of ₹18,000, a gain of about ₹2,000 before brokerage, charges, and taxes.

Important

This works only because two conditions were met: the company was fundamentally strong, and the investor managed her risk by investing in small parts. Without these two conditions, the same maths becomes a way to lose more money faster.

Educational example only

Wipro is used here only to make the example feel real. The prices ₹200 and ₹160 are illustrative round numbers, not actual market prices. This is not a recommendation to buy or sell Wipro or any stock. If actual live prices or financials of any company are added before publishing, they must be verified from official sources first.

How Averaging Reduces Your Purchase Price

Your average price is simply the total money you invested divided by the total number of shares you own. Every time you buy at a price lower than your current average, the average moves down. Every time you buy at a higher price, the average moves up. That is the whole formula:

Average Price = Total Amount Invested ÷ Total Shares Held

Why does a lower average matter? Because your profit or loss is always measured from your average price, not from your first purchase price. If your average is ₹180, the stock only needs to cross ₹180 (plus charges) for you to be in profit, instead of ₹200. This is exactly how to average stocks in a disciplined way.

Staged buying plan during a dip (illustrative)

Purchase Stage | Share Price | Amount Invested | Purpose |

|---|---|---|---|

First Purchase | ₹200 | Small amount | Initial entry after research |

After 20% Fall | ₹160 | Small additional amount | Reduce average price |

Another Fall | ₹140 (example) | Only if fundamentals are strong | Accumulate carefully, keep reserve cash |

Notice that at every stage the amount is small and the decision depends on a fresh check of the business, not on the price alone. Averaging is a tool, and like any tool, it helps when used with judgement and hurts when used blindly.

Why Every Fall Can Look Like an Opportunity

Long-term investors often say that market falls are when future returns are "created". There is truth in this. When a genuinely strong business falls in price for reasons unrelated to its own performance, a patient investor gets to own the same quality at a lower cost. The business has not become worse; only its price tag has.

Several situations can push good stocks down temporarily:

Market-wide fear: global events, wars, pandemic scares, or foreign investor selling can drag down almost every stock on the NSE and BSE, including excellent companies.

Temporary bad news: one weak quarter, a short-term margin squeeze, or a delayed order can cause sharp reactions even when the long-term story is intact.

Global corrections: when the US or other major markets fall, Indian markets often follow for some time, regardless of local company performance.

Sector weakness: an entire sector like IT, banking, or pharma may go out of favour for a while, pulling down both weak and strong companies within it.

In these cases, the fall is about mood and money flows, not about the company's engine. This is exactly why every fall looks like an opportunity. But here is the trap: a falling price alone tells you nothing about whether it is a genuine opportunity or the beginning of a permanent decline. Both look identical on the chart in the early days. The difference lies inside the business, and you can only see it through research.

When Buying the Dip Can Work Well

Buy the dip works best when the fall is temporary but the business is durable. Some signs that increase the odds in your favour:

Strong, understandable business: the company sells products or services that people will still need years from now, and you can explain how it earns money in one or two sentences.

Healthy financials: low or manageable debt, consistent sales, stable or growing profits, and positive cash flows over multiple years.

Trusted management: promoters and managers with a clean track record, transparent communication, and no history of governance problems.

Long-term sector tailwind: the industry itself is expected to grow with India's economy, such as areas linked to consumption, infrastructure, or digitisation.

Market-driven fall: the price drop is part of a broad share market correction or sector sell-off, not caused by damage inside this specific company.

You have holding power: the money invested is money you will not need for years, so you can wait through the recovery period without stress.

The pattern to remember

Good business + temporary fall + small staged purchases + long holding period is the only combination where buying on dips has historically made sense as a strategy. Remove any one ingredient and the risk rises sharply.

When Buying the Dip Can Be Dangerous

This is the section many beginners skip, and it is the most important one in this article. Not every fall is a discount. Some falls are warnings. Buying every falling stock is one of the fastest ways to destroy capital in the market.

Stocks can fall and never recover, or take a decade to recover, because of real problems:

Weak fundamentals: shrinking sales, falling profits, and losing customers. The price falls because the business is genuinely getting worse.

High debt: companies drowning in loans can see their equity value collapse. A "cheap" price can become cheaper and then almost worthless.

Fraud and poor governance: Indian market history has several painful cases where accounting fraud or promoter misconduct destroyed shareholder wealth permanently. In such cases, every dip was a trap, and every averaging purchase increased the loss.

Declining industry: some businesses are being replaced by technology or changing consumer habits. A falling price in a dying industry is usually fair, not a bargain.

The value trap: a stock that looks cheap on numbers but stays cheap or keeps falling because the market correctly sees a broken future.

Catching a falling knife: buying aggressively while a stock is crashing on serious negative news. Like a real falling knife, it is safer to let it hit the ground and stabilise than to grab it mid-air.

Emotional averaging: buying more only to "recover the loss" or to prove yourself right, without re-checking the business. This turns a small mistake into a large one.

The hard rule

If a stock is falling because the business itself is in trouble — bad results, rising debt, fraud allegations, exiting auditors, promoter pledging, regulatory action — averaging down does not reduce your risk. It multiplies it. In such situations, protecting your remaining capital matters more than reducing your average.

Buying the Dip vs Averaging Down: What is the Difference?

The two terms are related and often used together, but they are not identical. Buying the dip is a general strategy of purchasing after a fall. Averaging down specifically means adding to a stock you already own at prices below your existing average.

Two related ideas, one shared risk

Point | Buying the Dip | Averaging Down |

|---|---|---|

Meaning | Buying a stock after its price falls, whether or not you already own it | Buying more of a stock you already hold, after it falls below your buying price |

Best Used When | A strong stock has temporarily corrected and you want to start or add a position | You already own the stock, fundamentals remain strong, and the fall is market-driven |

Main Risk | The price can keep falling after you buy | You may keep increasing your loss and concentration in a weakening company |

In practice, both succeed or fail for the same reason: the quality of the underlying business. The label matters far less than the research behind the purchase.

Step-by-Step Method to Buy the Dip Carefully

If you want to use this strategy as an Indian retail investor, a disciplined process protects you far more than any prediction. Here is a practical, beginner-friendly method:

Shortlist quality first, price later. Prepare a small watchlist of fundamentally strong companies you understand, before any dip arrives. Decisions made calmly in advance are better than decisions made during panic.

Check the fundamentals again when the dip comes. Read the latest results, debt levels, and management commentary. Ask one question: has the business changed, or only the price?

Divide your capital into parts. Split the money meant for a stock into three or four portions. This single habit prevents the most common disaster: going all-in at the first fall.

Decide your buying levels in advance. For example, plan to add a portion after roughly a 15–20% fall, and another only after a further significant fall, and only if fundamentals still pass your check.

Never invest all your money at once. Keep reserve cash. Dips can go deeper and last longer than anyone expects.

Track business news, not just price. Follow company announcements, results, and credible news. A 30% fall with clean news is very different from a 30% fall with fraud headlines.

Set a risk limit per stock. Decide the maximum percentage of your portfolio one stock can occupy, and stop adding once you reach it, no matter how attractive the dip looks.

Write down your reason before every purchase. One line is enough. If your only reason is "it has fallen a lot", do not buy.

Avoid emotional buying. No revenge buying, no FOMO buying, no buying to feel better about an existing loss.

Checklist Before Buying Any Dip

Run through this list honestly before pressing the buy button. If several answers are "no" or "I don't know", the dip is not for you, at least not yet.

Common Mistakes Beginners Make While Buying the Dip

Most losses from this strategy come from a handful of repeated mistakes. Recognising them in advance is half the protection:

Buying only because the price is down. "It was ₹500, now it's ₹300, so it must be cheap" is not analysis. A stock can fall 40% and still be expensive if the business is broken.

Investing all money at the first dip. Beginners often empty their savings at the first 10% fall, and then watch helplessly as the stock falls another 20% with no money left to average.

Averaging weak or unknown stocks. Adding more to a low-quality company multiplies risk. Averaging is a privilege reserved for strong businesses only.

Ignoring the news behind the fall. Buying without reading why the stock fell is like buying a flat without asking why the seller is desperate.

Following social media tips. Telegram channels, WhatsApp forwards, and influencer videos shouting "best dip to buy" often benefit the tipper, not the follower.

Expecting quick profit. Recoveries can take months or years. People who buy dips expecting a bounce in a week usually sell in frustration exactly when patience was needed.

Not tracking the average and exposure. Many investors do not even know their average price or how concentrated they have become in one stock after repeated buying.

Best Approach for Indian Retail Investors

For most people in India who invest alongside a job or business, the healthiest way to use dips is inside a larger, disciplined plan rather than as a standalone trick:

Invest gradually, always. Whether the market is up or down, staged buying beats lump-sum bravado for most retail investors. Dips simply become the moments when your planned purchases fetch more value.

Diversify. Spread your money across several quality companies and sectors. Then no single dip, however deep, can seriously hurt you.

Keep a long-term mindset. India's economy and its listed businesses grow over years, not weeks. Stock market investing in India rewards holding power more than timing skill.

Learn business fundamentals. Basic reading of sales, profit, debt, and cash flow turns you from a price-watcher into an investor. This is the real "dip detector".

Borrow discipline from SIP and STP. Even in direct stocks, you can behave like an SIP investor: fixed small amounts, regular intervals, extra small purchases during meaningful corrections. This removes emotion from the process.

Avoid over-concentration. Repeated dip-buying in one favourite stock quietly builds dangerous concentration. Cap your exposure per stock and respect the cap.

Review your portfolio regularly. Once a quarter, check whether the reasons you bought each stock are still valid. Exit logic matters as much as entry logic.

Prefer mutual funds if direct research feels heavy. Many beginners are better served by diversified equity funds through SIP, where professional managers handle stock selection, while they slowly learn direct investing.

Can Buying the Dip Make You Profitable?

Yes, it can, and that is exactly the phrasing to remember: can, not will. Profit happens when two things line up. First, your buying during the dip genuinely reduces your average purchase price. Second, the stock actually recovers and rises above that average. If either fails, there is no profit.

Also remember that your real-world profit is smaller than the on-screen gain. Brokerage, exchange charges, STT, GST on charges, and capital gains tax all take their share. A stock recovering exactly to your average price still leaves you at a small net loss after costs. So the recovery must be meaningful, not marginal.

Finally, respect the two risks nobody can remove: business risk (the company may genuinely decline) and market risk (even good stocks can stay down for long periods when the whole market is weak). Time is the third silent cost: money stuck for years in a slow recovery has an opportunity cost too. Buying the dip is a probability-improving discipline, not a profit guarantee.

Conclusion

A DIP in the share market is simply a fall in price, and buying the dip is the strategy of purchasing quality stocks during such falls to lower your average cost and benefit from long-term recovery. The Wipro-style example shows the maths: buy at ₹200, add a small quantity at ₹160, and your average drops to ₹180, so a recovery to ₹200 puts you in profit instead of merely at break-even.

But the maths is the easy part. The hard part, and the part that decides whether you build wealth or destroy it, is judgement: knowing which falls are temporary discounts on strong businesses and which are honest warnings about broken ones. Buying the dip becomes powerful only when it is combined with real research, patient long-term holding, strict risk control through small staged purchases, and ruthless selectivity about company quality. Buy the business, not the fall.

FAQs

01 What is DIP in the share market?

A dip is a fall or correction in the price of a stock or the overall market from its recent level. For example, a stock falling from ₹200 to ₹160 has "dipped" by 20%.

02 What does buying the dip mean?

Buying the dip means purchasing or accumulating shares after their price has fallen, expecting the price to recover over the long term. It works as a strategy only when the company is fundamentally strong and the fall is temporary or market-driven.

03 Is buying the dip good for beginners?

It can be, but only with discipline. Beginners should first learn to check company fundamentals, invest in small parts instead of all at once, and stick to quality businesses. Without these habits, dip-buying often increases losses instead of reducing them.

04 How does averaging reduce stock price?

Averaging does not change the stock's market price; it reduces your average purchase price. Average price equals total money invested divided by total shares held. Buying additional shares below your current average pulls the average down, so the stock needs to rise less for you to break even.

05 Can I buy more shares whenever the price falls?

No, and this is a serious warning. Some stocks fall because of real problems like weak results, high debt, fraud, or a declining industry, and they may never recover. Buy more only when the business remains fundamentally strong, the fall looks temporary, and your total exposure to that stock stays within your risk limit.

06 Is buying the dip profitable?

It can be profitable if your average price falls and the stock later recovers above it, but there is no guarantee. Charges, taxes, holding time, business risk, and market risk all affect the final outcome. Treat it as a risk-managed strategy, not an assured-return method.

07 What is the biggest risk of buying the dip?

Averaging into a fundamentally weak or fraudulent company, sometimes called catching a falling knife or falling into a value trap. In such cases, every additional purchase increases your loss, and the stock may never return to your average price.

08 How much money should I invest during a dip?

Only a small, pre-decided portion at each stage. A common-sense approach is to divide the money planned for a stock into three or four parts and deploy them gradually at meaningfully lower levels, while keeping reserve cash. Never invest emergency funds or money you may need soon.

09 Is the Wipro at ₹200 and ₹160 example a buy recommendation?

No. It is only an educational example to explain averaging. The prices are illustrative round numbers, not live market prices. Investors should do their own research before investing in any stock.

10 Does this article need live fact-checking?

Yes, if live stock prices, financial results, valuations, or company updates are added before publishing, they must be verified from official and current sources such as NSE, BSE, or company filings.

1 comment

nice